Why Should I Add Real Estate To My Portfolio?

Real estate investing is an excellent way to diversify your portfolio and reduce overall risk. Unlike stocks and bonds, real estate is not correlated with other asset classes, which means that adding it to your portfolio can help balance out your investments.

One of the most significant benefits of investing in real estate is the steady income it can provide. Rental income from properties can be used to supplement regular income or reinvested for growth. This makes real estate a great option for those looking for a reliable source of passive income.

In addition to providing steady rental income, real estate investments also act as an inflation hedge. As rental income and property values tend to increase with inflation, investing in real estate can help protect against the effects of rising prices.

Real estate is also a tangible asset that you can see and touch, unlike stocks and bonds. This provides investors with a sense of security and stability that cannot be found in other types of investments.

Finally, there is potential for capital appreciation over time when investing in real estate. If the property is sold at a higher price than it was purchased for, investors can realize significant returns on their investment.

Are you a medical professional striving for financial freedom in an uncertain economy? Red Pill Kapital is here to guide you through the complexities of contrarian real estate investing. Our specialized approach focuses on asymmetric returns, ensuring that your hard-earned wealth is safeguarded against market fluctuations, government instability, and high taxes. As a physician or high net-worth professional, your expertise and dedication to your patients deserve to be rewarded with financial security. By partnering with Red Pill Kapital, you’ll benefit from our unrivaled experience in managing commercial real estate, rental properties, and land speculation projects, all while maintaining your role as a Limited Partner (LP). We shoulder the responsibility as the General Partner (GP), allowing you to focus on your career while we grow your wealth. Embrace the opportunity to protect and expand your financial future through strategic real estate investments – visit www.redpillkapital.com and experience the extraordinary advantages of joining forces with Red Pill Kapital.

Introduction to Real Estate Investment

Real estate investment is a popular way for investors to generate income or profit through the appreciation of property values over time. There are many forms of real estate investments, including owning rental properties, investing in real estate projects, or joining a real estate investment group.

One of the benefits of investing in real estate is equity build-up. Property values typically increase over time, which means that investors can benefit from an appreciation in value. Additionally, rental income can provide a steady stream of cash flow.

Real estate is often considered a stable asset class that can help diversify an investment portfolio and hedge against inflation. Unlike stocks and bonds, which are subject to market volatility, real estate values tend to be more stable over the long term.

Accredited investors may have access to more lucrative real estate investment opportunities than non-accredited investors. For example, they may be able to invest in private equity funds or participate in syndicated deals with other accredited investors.

However, all investors should carefully consider their investment strategy and the price and potential returns of any properties they are considering investing in. It’s important to do your due diligence before making any investment decisions.

One way to invest in real estate is by owning rental properties. This involves purchasing a property and renting it out to tenants for monthly rent payments. The goal is to generate enough rental income to cover expenses like mortgage payments, property taxes, insurance premiums, and maintenance costs while also generating a profit.

Another form of real estate investment is investing in real estate projects. This involves investing money into a development project such as building new homes or commercial buildings with the expectation that the value will appreciate over time as construction progresses.

Investing in a Real Estate Investment Group (REIG) allows individuals who want exposure to real estate investments but don’t want the hassle of managing their own properties or projects directly. A REIG pools money from multiple investors who then use this capital collectively on various types of investments such as rental properties or development projects.

As with any investment, it’s important to have a clear investment strategy before investing in real estate. This includes determining your risk tolerance, understanding the potential returns and risks associated with different types of investments, and having a plan for managing your portfolio over time.

Real estate investors should also be aware of market trends and conditions. For example, if interest rates are rising, this can impact the affordability of mortgages and may make it more difficult to sell properties. Similarly, changes in zoning laws or economic conditions can impact the value of properties over time.

In addition to these considerations, investors should also be aware of the tax implications of real estate investments. Rental income is typically subject to income tax at both the federal and state level, while capital gains taxes may apply when selling properties that have appreciated in value.

Despite these challenges, real estate remains an attractive asset class for many investors due to its potential for long-term appreciation and steady cash flow through rental income. By carefully considering their investment strategy and doing their due diligence on potential investments, investors can benefit from this stable asset class as part of a diversified investment portfolio.

Understanding the Basics of Real Estate Investment

Positive cash flow is the ultimate goal of real estate investment. It is the net income generated by a property after all expenses have been paid. This means that rental income should exceed expenses to achieve positive cash flow, while negative cash flow occurs when expenses exceed rental income. Investors should aim for positive cash flow to ensure the profitability and sustainability of their investment.

Location plays a crucial role in determining the cash flow of a property. A good location with high demand can lead to higher rental rates, resulting in positive cash flow. On the other hand, a poor location with low demand can lead to lower rental rates and negative cash flow.

Market demand is another factor that affects the cash flow of a property. Properties located in areas with high market demand tend to generate more rental income, leading to positive cash flow. However, properties located in areas with low market demand may struggle to attract tenants and generate sufficient rental income.

Maintenance costs are also an important consideration when calculating cash flow. Properties that require frequent repairs or maintenance may incur higher expenses, leading to negative cash flow. It is essential for investors to factor in these costs when evaluating potential investments.

Understanding cash flow is crucial in making informed decisions when investing in real estate. Positive cash flow ensures profitability and sustainability of an investment, while negative cash flow can result in financial losses.

Investors should conduct thorough research before investing in any property. They should analyze the local market conditions, evaluate potential risks and returns, and calculate projected expenses and income streams.

One way investors can increase their chances of achieving positive cash flow is by purchasing undervalued properties that require minimal renovations or repairs but have high potential for rental income growth.

Another strategy is to invest in multifamily properties such as apartment complexes or duplexes which offer multiple streams of rental income from several units within one building or complex.

Real estate investment trusts (REITs) are another option for investors who want exposure to real estate without owning physical property. REITs are companies that own and operate income-generating real estate properties such as apartments, hotels, or office buildings. Investors can purchase shares in a REIT and receive a portion of the rental income generated by the properties owned by the trust.

Exploring Different Types of Real Estate Investments

Rental Properties: A Stable and Long-Term Investment

One of the most popular types of real estate investments is rental properties. Investors purchase a property with the intention of renting it out to tenants for a steady stream of income. This type of investment can be particularly attractive for those looking for long-term stability in their portfolio.

Rental properties come in many forms, from single-family homes to multi-unit apartment buildings. Investors should carefully consider the location, condition, and potential rental income when selecting a property. They should also factor in expenses such as property taxes, maintenance costs, and vacancies.

One advantage of rental properties is that they provide consistent cash flow over time. As long as there are tenants occupying the property, investors can expect to receive monthly rent payments. Additionally, rental properties have the potential to appreciate in value over time, providing an opportunity for capital gains.

However, owning a rental property also comes with its own set of challenges. Landlords must deal with tenant turnover, repairs and maintenance issues, and legal requirements such as eviction procedures. It’s important for investors to have a solid understanding of landlord-tenant laws and regulations before diving into this type of investment.

Fix-and-Flip Properties: A High-Risk but Potentially Lucrative Investment

Real estate flippers buy distressed properties with the intention of renovating them quickly and reselling them at a profit. This type of investment requires significant capital upfront to purchase and renovate the property, as well as expertise in construction and design.

The goal is to make quick profits by buying low and selling high within a short period – usually within 6 months or less – after renovation work has been completed on the property.

While fix-and-flip investments can be highly lucrative if done correctly, they are also among the riskiest types of real estate investing due to their high level of volatility – both in terms of market conditions (such as interest rates) which can affect the sale price of the property, and in terms of unforeseen expenses that can arise during renovation work.

Commercial Real Estate: A Diversified Investment

Commercial real estate investments involve purchasing properties used for business purposes, such as office buildings, retail spaces, or warehouses. This type of investment can be attractive to those looking for a more diversified portfolio beyond residential properties.

Investors should carefully consider factors such as location, tenant mix, and market demand when selecting a commercial property. They should also factor in expenses such as property taxes and maintenance costs.

One advantage of commercial real estate is that it typically provides higher rental income than residential properties due to longer lease terms and higher rents. Additionally, commercial properties often have multiple tenants, providing a more stable source of income even if one tenant leaves.

However, investing in commercial real estate also comes with its own set of challenges. Investors must deal with complex leasing agreements and tenant management issues. Additionally, vacancy rates can be higher than residential properties due to economic downturns or shifts in consumer behavior.

Land Speculation: A High-Risk Investment

Land speculation involves buying undeveloped land with the expectation that its value will increase over time. This type of investment can be highly speculative and risky since it depends on unpredictable factors such as zoning laws, infrastructure development, and market demand.

Investors should carefully consider the potential risks associated with owning undeveloped land before making an investment decision. Holding costs associated with owning undeveloped land are another factor investors need to consider – these include property taxes and maintenance fees which can add up quickly over time.

While land speculation has the potential for high returns if done correctly – especially if there is significant development activity happening nearby – it’s important for investors to approach this type of investment with caution due to its high level of risk.

Finding the Right Real Estate Investment for You

Determine Your Investment Goals and Risk Tolerance

Before investing in real estate, it’s important to determine your investment goals and risk tolerance. This will help you find the right type of investment property for you. Are you looking for a long-term investment or a short-term flip? Do you want to invest in a single-family home, multi-unit building, or commercial property?

Your risk tolerance is also an important factor to consider. Real estate investments can be risky, so it’s essential to assess how much risk you’re willing to take on. If you’re new to real estate investing, it may be best to start with a less risky option like a single-family home.

Utilize Online Real Estate Platforms

Once you’ve determined your investment goals and risk tolerance, the next step is to utilize online real estate platforms. These platforms allow you to research potential properties and compare prices and returns on investment.

One popular platform is Zillow, which provides information on homes for sale as well as estimated home values. Redfin is another popular platform that offers detailed information on homes for sale and recently sold properties.

Consider Working with a Property Manager

Investing in real estate requires ongoing management of the property. If you don’t have the time or expertise to manage the property yourself, consider working with a property manager.

A property manager can help with the buying process by providing insights into the local market and negotiating deals on your behalf. They can also handle ongoing management tasks like rent collection, maintenance requests, and tenant screening.

Evaluate Your Skills and Resources

Before deciding whether to invest in a rehab project or work with experienced flippers, evaluate your skills and resources. Rehab projects require significant time and money investments, so it’s important to have experience in construction or renovation before taking on such projects.

Working with experienced flippers can be beneficial if you lack experience but have financial resources available for investment. Flippers typically purchase distressed properties at a low price, renovate them, and sell them for a profit.

Look for Properties with Potential for Equity Growth

When searching for investment properties, look for properties with potential for equity growth. This means that the property has the potential to increase in value over time.

Properties located in up-and-coming neighborhoods or areas experiencing economic growth are often good options. Additionally, properties that require minor renovations or updates can also provide opportunities for equity growth.

High Returns on Investment

In addition to equity growth potential, it’s important to consider the returns on investment when evaluating investment properties. Look for properties that offer high returns on investment.

One way to calculate returns on investment is by using the cap rate formula. The cap rate is calculated by dividing the net operating income (NOI) by the purchase price of the property. A higher cap rate indicates a better return on investment.

Best Ways to Find Investment Properties

There are several ways to find investment properties beyond online real estate platforms. One option is attending local real estate auctions where distressed properties are sold at a discounted price.

Networking with other real estate investors can also be beneficial as they may have insights into upcoming deals or off-market opportunities.

Commercial Real Estate: A Lucrative Investment Opportunity

Maximizing Profit Potential with Commercial Real Estate

Commercial real estate can provide a higher profit potential compared to residential properties due to larger market values and rental rates. Investing in commercial real estate can be a lucrative opportunity for those looking for long-term profits.

The Real Estate Market for Office Buildings

The real estate market for office buildings has been steadily growing, making it a stable investment option for long-term profits. With the increase in remote work, there may be some concerns about the demand for office space, but many businesses still require physical locations to operate. Additionally, the shift towards shared workspaces and flexible leasing options can help mitigate any potential risks.

Investing in Land for Commercial Development

Investing in land for commercial development can also be a lucrative opportunity, as the value of the property can increase significantly over time. However, this type of investment requires careful consideration and research into zoning regulations and potential development plans in the surrounding area.

Proper Management is Crucial

Proper management is crucial in maximizing profits from commercial real estate investments. This includes maintaining tenant relationships and optimizing rental rates. Short-term leases can provide flexibility in a changing market, but long-term leases with reliable tenants can ensure steady income streams.

Market Conditions Matter

It’s important to consider the overall market conditions when investing in commercial real estate. Economic trends and local regulations may impact the property’s value and potential profits. For example, changes in interest rates or tax laws could affect financing options or operating costs.

Case Study: The Empire State Building

One notable example of successful commercial real estate investment is the Empire State Building. Originally purchased during the Great Depression at a fraction of its current value, it was renovated and marketed as an office building with high-end amenities such as air conditioning and private bathrooms. Today, it remains one of New York City’s most iconic landmarks and profitable commercial properties.

Social Proof: Top 10 Richest Real Estate Investors

According to Forbes, the top 10 richest real estate investors in the world have a combined net worth of over $100 billion. This includes individuals who have made their fortunes through commercial real estate investments, such as Brookfield Asset Management CEO Bruce Flatt and Blackstone Group founder Stephen Schwarzman.

Investing in Rental Properties: Small-Scale and Large-Scale Options

Small-Scale Rental Properties: A Steady Source of Income

Rental properties can be a great investment option, providing regular income through rent payments. Small-scale rental properties may require less upfront costs and can provide a steady source of income. Financing options are available for small-scale rental projects, with monthly payments spread out over the long term.

When investing in small-scale rental properties, it’s important to consider the potential rental rates in the area. Researching the average rental rates in the neighborhood can help investors determine how much they can charge for rent and what kind of return they can expect on their investment.

In addition to rental income, there may be other sources of revenue from small-scale rental properties. For example, parking or laundry facilities could provide an additional stream of income for property owners.

Large-Scale Rental Projects: Potential for Higher Returns

While small-scale rental properties offer a steady source of income, large-scale projects have the potential for higher returns but may require more capital upfront. Financing options are also available for large-scale projects, with monthly payments spread out over the long term.

When considering large-scale rental projects, it’s important to evaluate potential sources of income beyond just rent payments. For example, commercial spaces within a larger property could generate additional revenue streams.

It’s also important to consider any associated costs with large-scale projects. Upfront costs such as construction or renovation expenses should be factored into an investor’s overall strategy before making any decisions.

Developing a Rental Property Investment Strategy

Whether investing in small or large scale rental properties, developing a solid investment strategy is key to success. Investors should carefully evaluate potential sources of revenue and associated costs when making decisions about which projects to pursue.

Researching local real estate market trends and analyzing comparable sales data can help investors make informed decisions about where to invest their money. Additionally, working with experienced real estate professionals such as agents or property managers can provide valuable insights into local market conditions and help investors make more informed decisions.

With the ability to generate passive income and potentially appreciate in value over time, investing in rental properties can be a smart long-term investment option. However, it’s important for investors to carefully evaluate potential costs and revenue streams before making any decisions. By developing a solid investment strategy and working with experienced professionals, investors can maximize their returns on rental property investments.

Transform Your Financial Future: Medical Professionals Thriving in an Era of High Taxes with Red Pill Kapital Don’t let increasing tax rates jeopardize your hard-earned wealth. As a medical professional, team up with Red Pill Kapital as a Limited Partner (LP) and experience the power of contrarian real estate investing. Our General Partner (GP) role ensures expert management of your investments, safeguarding your financial future amid economic uncertainty.

Real Estate Investment Trusts (REITs): A Passive Investment Option

Traded REITs are publicly traded companies that own and manage income-producing real estate properties, making them an attractive investment option for individual investors. These companies are required by law to distribute at least 90% of their taxable income to shareholders in the form of dividends, making them a popular choice for income-seeking investors.

One advantage of investing in REITs is their liquidity. Traded REITs are listed on major stock exchanges, which means that they can be bought and sold like any other stock. This makes it easy for individual investors to invest in real estate without having to buy physical property themselves.

Another benefit of investing in REITs is diversification. Because these companies own and manage a portfolio of properties across different sectors and geographic regions, they offer exposure to a variety of real estate markets. This can help reduce risk and volatility in an investor’s portfolio.

In addition to traded REITs, there are also mutual funds that invest in a diversified portfolio of REITs. These funds provide a passive investment option for those looking to add real estate exposure to their investment portfolio without having to actively manage individual investments.

Investing in traded REITs or mutual funds that invest in REITs can be a great way for individuals to gain exposure to the real estate market while also enjoying the benefits of liquidity and diversification. However, it’s important for investors to do their due diligence before investing in any particular company or fund.

When considering an investment in a traded REIT or mutual fund that invests in REITs, investors should look at factors such as the company’s track record, management team, dividend history, and overall financial health. They should also consider factors such as the fees associated with the investment and how well it fits into their overall investment strategy.

One potential downside of investing in traded REITs is that they can be sensitive to interest rate changes. When interest rates rise, the cost of borrowing money to purchase properties increases, which can put pressure on the profitability of REITs. However, this risk can be mitigated by investing in a diversified portfolio of REITs across different sectors and geographic regions.

Preserve Your Wealth as a Medical Professional: Leverage Red Pill Kapital’s Contrarian Real Estate Expertise With tax rates climbing, it’s crucial for physicians and high net-worth professionals to safeguard their wealth. Join forces with Red Pill Kapital as a Limited Partner (LP) and benefit from our General Partner (GP) expertise in contrarian real estate investing, ensuring your financial security in an ever-changing economic landscape.

Crowdfunding Real Estate Platforms: Understanding the Risks

Understanding the Risks of Crowdfunding Real Estate Platforms

Real estate crowdfunding platforms have become increasingly popular in recent years, allowing investors to pool their money together to invest in real estate projects. While these platforms offer a new and exciting way for investors to get involved in real estate investments, it’s important to understand the risks involved.

Lack of Regulation on Online Real Estate Platforms

One of the biggest risks associated with investing in online real estate platforms is the lack of regulation. Unlike traditional real estate investments, which are heavily regulated by government agencies, online real estate platforms may not have the same level of oversight or regulation.

This means that investors need to do their due diligence before investing in any platform. They should research the platform thoroughly and make sure that it has a good reputation and track record.

Potential High Returns vs. Risk of Losing Investment

Another risk associated with crowdfunding real estate platforms is the potential for high returns versus the risk of losing your investment. These platforms can offer potentially high returns, but they also come with a higher level of risk than traditional investments.

Investors should be aware that they may face the risk of losing their entire investment if the project does not perform as expected. This could happen if there are unexpected delays or cost overruns during construction or if there is a downturn in the real estate market.

Diversification Can Help Mitigate Risk

One way to mitigate some of these risks is through diversification. By spreading your investments across multiple projects on different crowdfunding platforms, you can help reduce your overall risk exposure.

However, it’s important to keep in mind that diversification alone cannot eliminate all risks associated with investing in crowdfunding real estate platforms.

Due Diligence Is Key

Ultimately, due diligence is key when investing in any type of investment opportunity, including crowdfunding real estate platforms. Investors should carefully review all available information about a platform and its projects before making any investment decisions.

This includes reviewing financial statements, project plans, and any other relevant information that may be available. Investors should also consider seeking advice from a financial advisor or other professional before making any investment decisions.

Maximize Your Returns, Minimize Your Taxes: Red Pill Kapital’s Real Estate Solutions for Medical Professionals As a physician or high net-worth professional, the threat of increasing taxes can weigh heavily on your financial future. Secure your wealth with Red Pill Kapital as a Limited Partner (LP) and let our General Partner (GP) expertise in contrarian real estate investing shield your assets from the adverse effects of rising tax rates.

Final Thoughts on Real Estate Investment

Real estate investment is a lucrative option for those looking to diversify their portfolio and generate passive income. By investing in real estate, you can benefit from price appreciation and magnified returns, making it an attractive option for many investors.

However, before diving into the world of real estate investment, it’s important to understand the basics. You should explore different types of investments and find the right one that suits your goals and preferences. Whether you’re interested in commercial real estate or rental properties, there are many options available.

One popular option is commercial real estate. This type of investment can provide high returns but requires significant capital upfront. Investing in rental properties is another option that allows for both small-scale and large-scale investments. With rental properties, you can generate passive income through rent payments while also benefiting from price appreciation over time.

For those who prefer a more passive approach to investing, Real Estate Investment Trusts (REITs) offer a great alternative. REITs allow investors to invest in a diversified portfolio of real estate assets without having to manage them directly.

Investing in your own home is also a smart financial move as it provides long-term benefits such as equity growth and potential price appreciation over time.

Lastly, crowdfunding real estate platforms offer another avenue for investors to participate in real estate projects with lower capital requirements than traditional investments. However, it’s important to understand the risks involved before investing in these platforms.

Gain Financial Stability in a High-Tax World: Medical Professionals Thriving with Red Pill Kapital’s Real Estate Strategies Rising tax rates can endanger the financial stability of physicians and high net-worth professionals. Protect your wealth by partnering with Red Pill Kapital as a Limited Partner (LP) and let our General Partner (GP) expertise in contrarian real estate investing fortify your financial future, ensuring long-lasting prosperity in an uncertain economic environment.

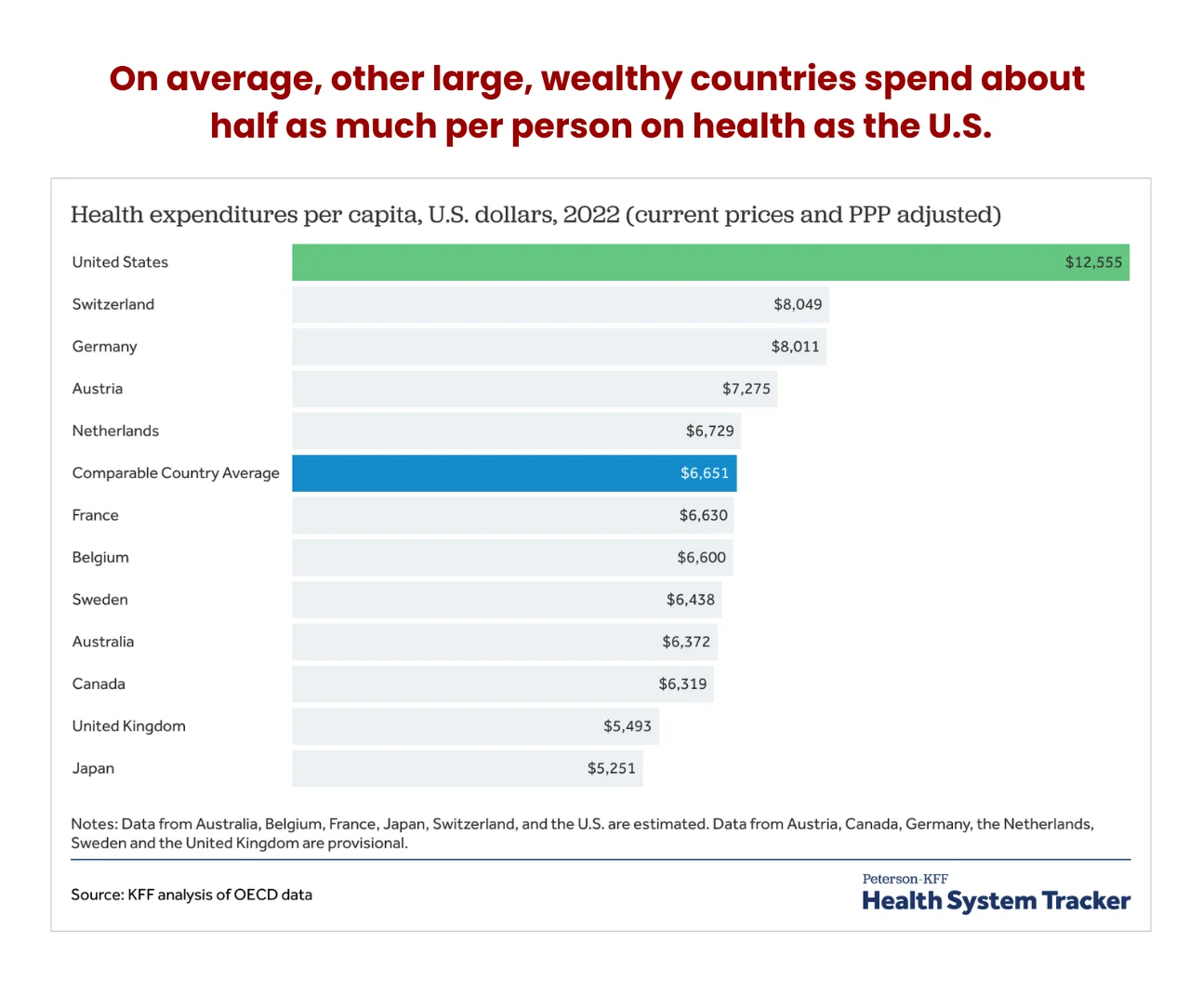

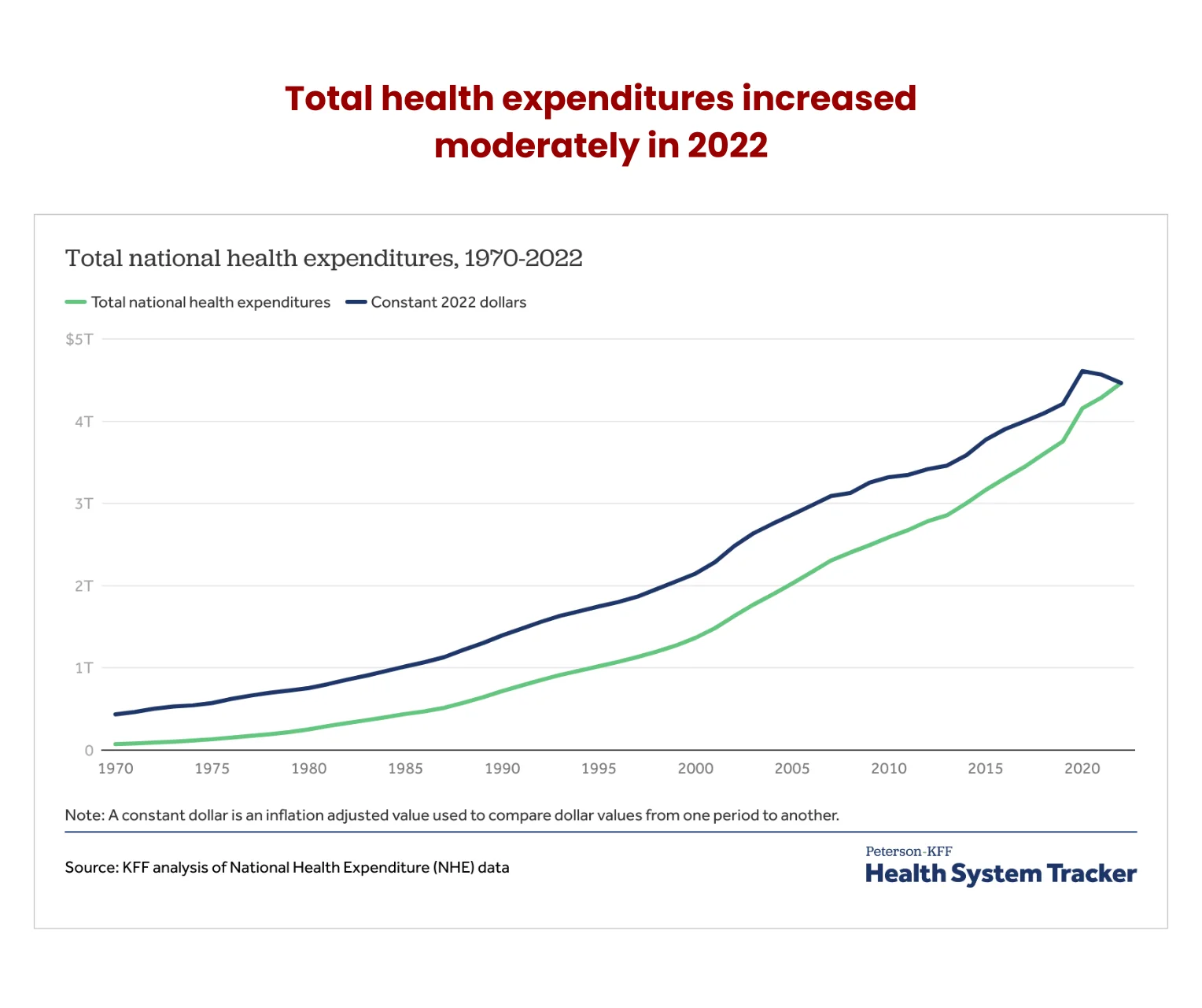

What does this mean, and how does this affect physicians? This article examines the economic pressures influencing health spending and how it impacts physicians. It also provides valuable strategies physicians can implement to combat the adverse effects of these healthcare spending trends.

What does this mean, and how does this affect physicians? This article examines the economic pressures influencing health spending and how it impacts physicians. It also provides valuable strategies physicians can implement to combat the adverse effects of these healthcare spending trends. And hospital bills on a per-person basis have followed the same trajectory, rising 3,100%. Healthcare costs were $353 in 1970 compared to $11,453 in 2019, adjusted for inflation.

And hospital bills on a per-person basis have followed the same trajectory, rising 3,100%. Healthcare costs were $353 in 1970 compared to $11,453 in 2019, adjusted for inflation.

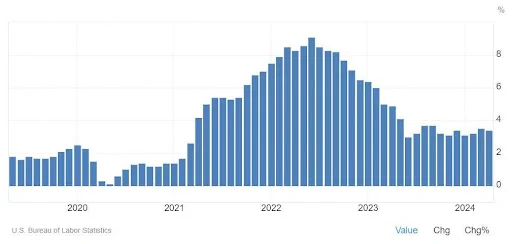

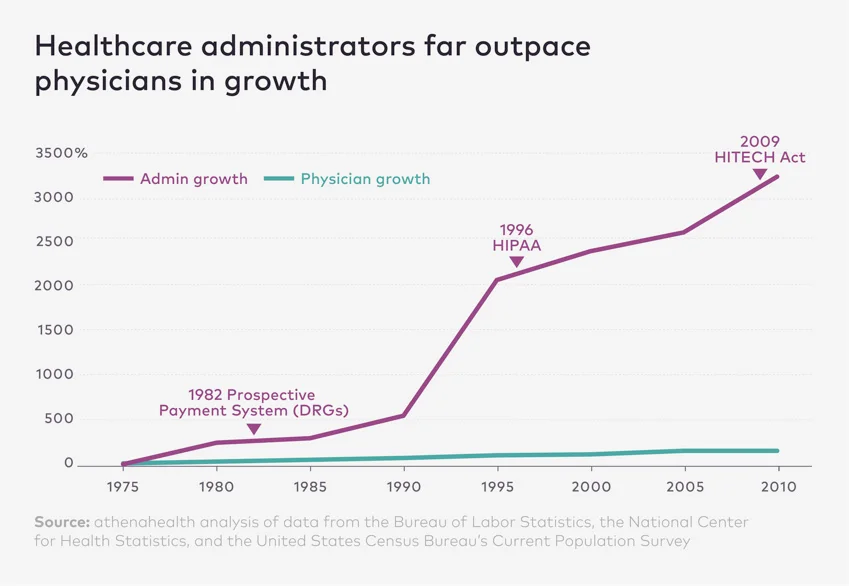

Health insurance CPI dipped from an all-time-high annual increase of 28.2% in September 2022 to -24.9% in June 2023. Overall, medical care prices realized the slowest decades-long price gain in June 2023.In 2024, BLS data shows the CPI-U for medical care services index went up by 0.6% in March, up from the -0.1% recorded in February. Medical care commodities were up 0.2% in March, higher than the 0.1% recorded the previous month, although this is not seasonally adjusted.

Health insurance CPI dipped from an all-time-high annual increase of 28.2% in September 2022 to -24.9% in June 2023. Overall, medical care prices realized the slowest decades-long price gain in June 2023.In 2024, BLS data shows the CPI-U for medical care services index went up by 0.6% in March, up from the -0.1% recorded in February. Medical care commodities were up 0.2% in March, higher than the 0.1% recorded the previous month, although this is not seasonally adjusted.